Are Wall Street Analysts Predicting Vistra Stock Will Climb or Sink?

Irving, Texas-based Vistra Corp. (VST) operates as an integrated retail electricity and power generation company. With a market cap of $64.5 billion, the company is also involved in wholesale energy purchases and sales, commodity risk management, fuel production, and fuel logistics management activities.

Shares of the leading integrated retail electricity and power generation company have considerably outperformed the broader market over the past year. VST has gained 128.6% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 16.1%. In 2025, VST stock is up 38.1%, surpassing the SPX’s 10% rise on a YTD basis.

Zooming in further, VST’s outperformance is also apparent compared to the iShares U.S. Utilities ETF (IDU). The exchange-traded fund has gained about 14.2% over the past year. Moreover, VST’s gains on a YTD basis outshine the ETF’s 13.9% returns over the same time frame.

Vistra’s outperformance stems from its strategic position in the U.S. energy transition, driven by its advanced energy storage systems, diversified portfolio of renewables, gas, and storage assets, and expansion of clean energy projects. The company's acquisition of natural gas facilities also positions it to meet rising demand from AI data centers, solidifying its role as a reliable power provider in a market increasingly focused on stability and decarbonization.

On Aug. 7, VST shares closed up more than 2% after reporting its Q2 results. Its revenue advanced 10.5% year-over-year to $4.3 billion. The company’s adjusted EBITDA stood at $1.3 billion, down 4.5% from the year-ago quarter.

For the current fiscal year, ending in December, analysts expect VST’s EPS to decline 10% to $6.30 on a diluted basis. The company’s earnings surprise history is mixed. It beat or matched the consensus estimate in three of the last four quarters while missing the forecast on another occasion.

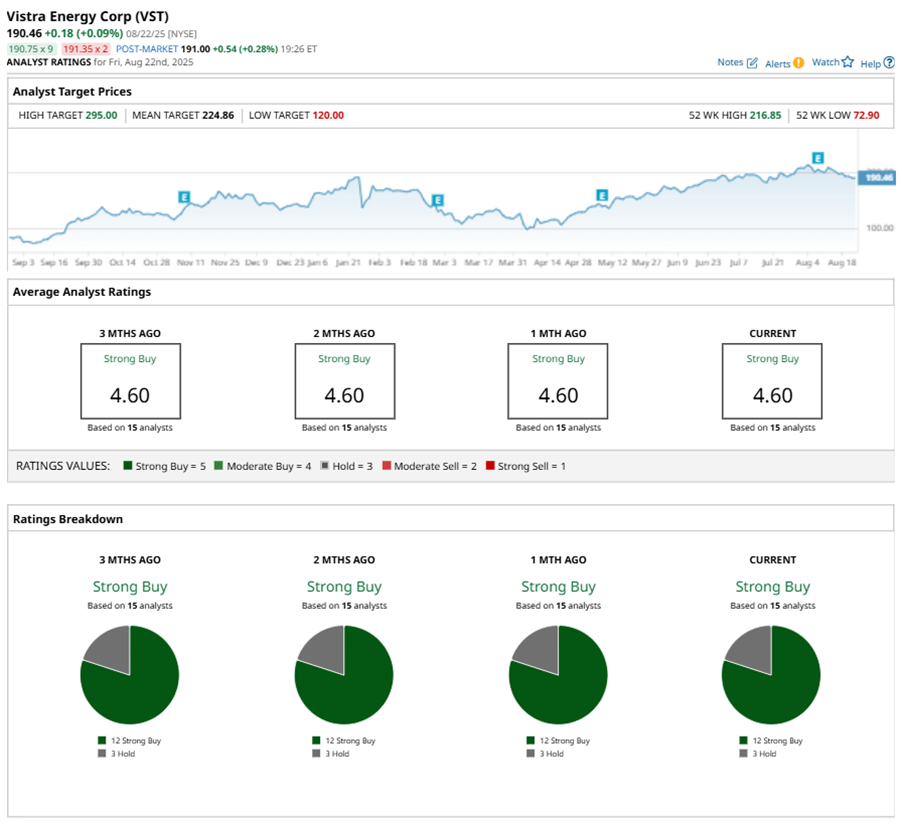

Among the 15 analysts covering VST stock, the consensus is a “Strong Buy.” That’s based on 12 “Strong Buy” ratings, and three “Holds.”

The configuration has been consistent over the past three months.

On Aug. 21, Morgan Stanley (MS) analyst David Arcaro kept an “Overweight” rating on VST and raised the price target to $207, implying a potential upside of 8.7% from current levels.

The mean price target of $224.86 represents an 18.1% premium to VST’s current price levels. The Street-high price target of $295 suggests an ambitious upside potential of 54.9%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.